Uganda’s domestic debt market is undergoing a structural shift, with pension and provident funds emerging as the single largest holders of government securities, overtaking commercial banks in a development that signals deepening institutional participation in public finance.

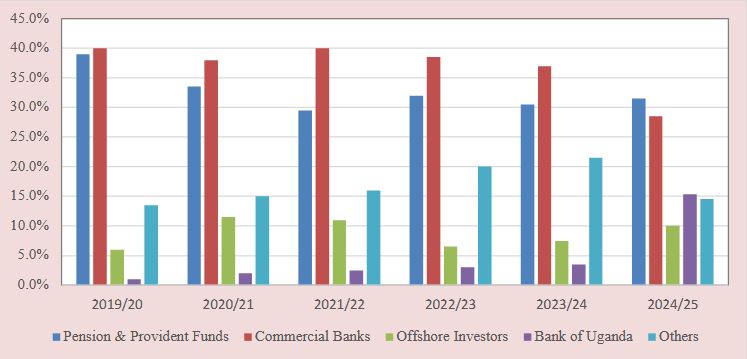

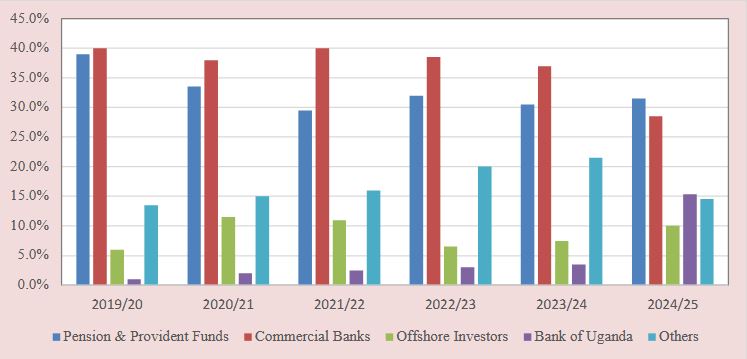

As at June 2024, pension and provident funds accounted for 48.3 percent of domestic public debt, surpassing commercial banks, whose share declined to 26.4 percent. The rebalancing marks a notable evolution in the composition of investors financing government operations, particularly at a time when global financing conditions have tightened and external borrowing has become more costly.

Domestic debt surpasses external debt

The shift in investor composition has coincided with a broader restructuring of Uganda’s public debt portfolio. In FY 2023/24, domestic debt overtook external debt as the dominant component of total public debt. Domestic debt accounted for 52.9 percent of total public debt at end-June 2024, up from 48.6 percent in the previous financial year, while the share of external debt declined to 47.1 percent.

Total public debt rose during the financial year, driven largely by domestic borrowing. The increase reflected higher fiscal deficits, increased development spending—particularly in preparation for oil production—and the securitisation of central bank advances.

The growing reliance on domestic borrowing has placed greater emphasis on the structure and stability of the local investor base. Pension funds’ rise to dominance suggests that long-term institutional capital is increasingly anchoring government financing.

Why pension funds are gaining ground

Analysts attribute the rise of pension and provident funds to several factors. Uganda’s retirement savings sector has expanded steadily, supported by enhanced sensitisation of individuals and firms to invest through institutional channels. As assets under management grow, pension funds require stable, long-duration instruments to match their liabilities.

Government securities—particularly treasury bonds—have become a natural fit.

Over the years, authorities have deliberately lengthened the maturity profile of domestic debt to reduce refinancing risk and smooth the redemption schedule. Treasury bonds now account for nearly four-fifths of domestic debt stock, while short-term treasury bills make up the remainder.

For pension funds, long-term bonds align closely with their obligation to meet future retirement payouts. For government, the shift reduces rollover pressures and limits exposure to short-term interest rate volatility.

Commercial banks, by contrast, operate under tighter liquidity and capital constraints and must balance holdings of government paper with private sector lending. While banks remain significant investors in government securities, their relative share has declined as pension assets expand more rapidly.

Implications for credit and liquidity

The rebalancing of domestic debt holdings may have important implications for private sector credit.

With commercial banks holding a smaller proportion of government securities, there is potential for more balance sheet space to be directed toward lending to businesses and households. However, this outcome will depend on prevailing interest rates, risk appetite and macroeconomic stability.

Debt servicing pressures remain elevated. As at June 2024, debt service absorbed 48.9 percent of domestic revenues, and the ratio is projected to peak above 50 percent in the coming year before gradually declining. Elevated domestic interest rates and tighter global financial conditions continue to exert upward pressure on borrowing costs.

In this environment, the stability of pension fund financing provides some buffer against sudden shifts in market sentiment. Pension funds, unlike more short-term investors, are less prone to rapid portfolio reallocation in response to temporary market fluctuations.

Central bank and offshore participation

Holdings by the Bank of Uganda increased significantly during the year, rising from 4.3 percent to 14.7 percent of domestic debt following the securitisation of advances extended to government. While this was largely a technical adjustment, it contributed to changes in the overall distribution of debt holdings.

Meanwhile, offshore investors maintained a modest but growing presence, holding about 10 percent of domestic debt. Their participation underscores continued foreign interest in Uganda’s government securities market, even amid global uncertainty.

Debt sustainability and the medium-term outlook

Uganda’s Debt Sustainability Analysis indicates that public debt remains sustainable over the medium to long term, supported by fiscal consolidation efforts, domestic revenue mobilisation, and anticipated oil-related revenues. However, risks remain elevated, particularly in the context of high debt service burdens and vulnerability to external shocks.

Real GDP growth and currency appreciation helped moderate the increase in the debt-to-GDP ratio during the financial year, partially offsetting the impact of higher deficits and interest costs. Economic growth strengthened to above 6 percent in FY 2023/24, providing some support to debt dynamics.

Looking ahead, concessional external financing is expected to decline as Uganda progresses toward middle-income status, further increasing the importance of a robust domestic investor base.

The emergence of pension funds as the dominant holders of government debt therefore represents more than a statistical milestone. It signals the maturation of Uganda’s domestic capital market and the growing role of long-term institutional savings in financing the state.

For policymakers, the challenge will be to leverage this deepening institutional base while maintaining fiscal discipline. For investors and economists, the shift offers a window into how Uganda is adapting its financing model in an era of constrained global capital and rising domestic funding needs.